Why Property Managers Are Dumping Bank Loans for Merchant Cash Advances

I. Introduction: The Property Manager’s Modern Dilemma

Let’s face it—property management is more than collecting rent. It’s solving problems before they become disasters. HVAC failures, leaky roofs, broken elevators, or a sudden tenant move-out can all hit your bottom line. But when you need fast capital to cover repairs, renovations, or seasonal income gaps, where do you turn?

Traditionally, the answer was the bank. But for modern-day property managers juggling multiple tenants, contracts, and cash flow complexities, banks are increasingly out of step. The application process is long. The requirements are strict. And the approval? Not guaranteed.

That’s why more and more property managers are saying goodbye to bank loans—and turning to a faster, more flexible solution: the Merchant Cash Advance (MCA).

This article explores why MCAs are becoming the go-to option for real estate professionals, how they compare to traditional loans, and how they help landlords stay liquid, agile, and in control.

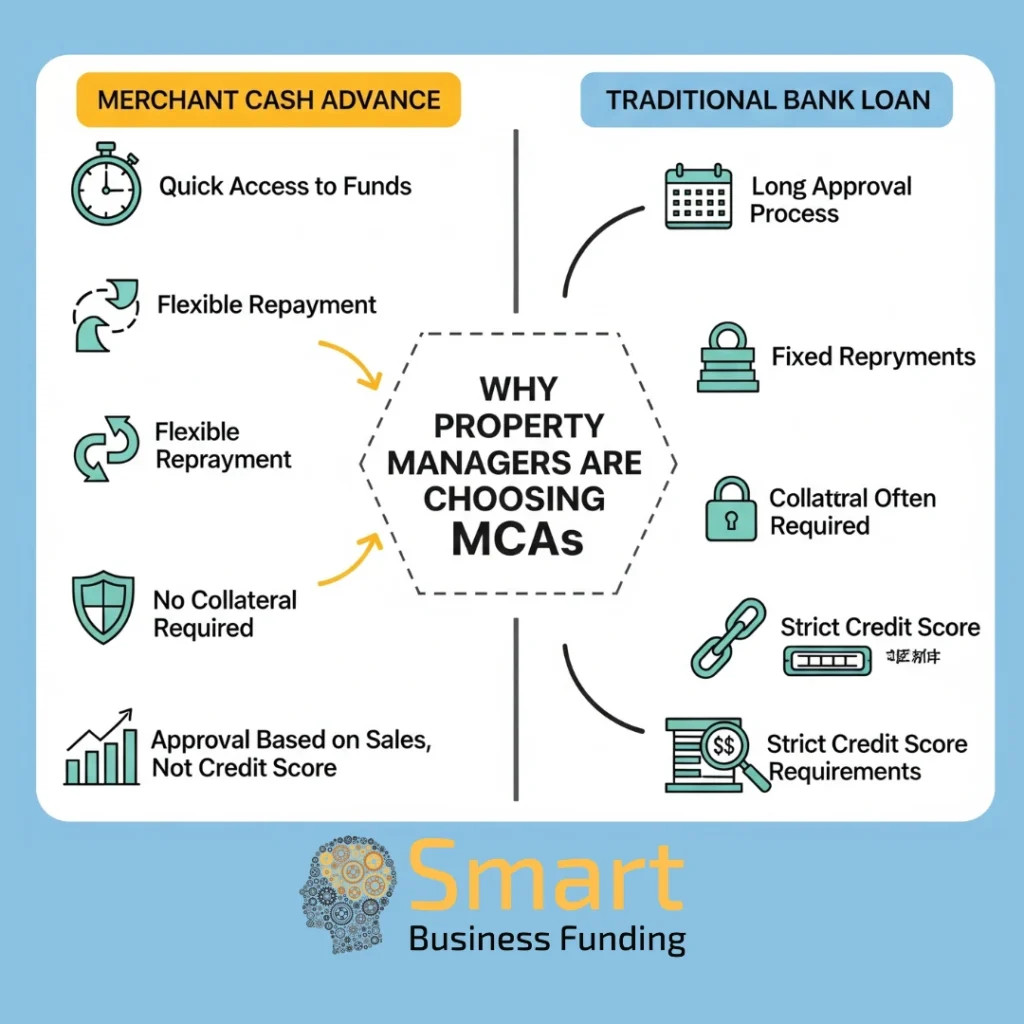

II. The Reality of Bank Loans for Property Managers

Traditional bank financing has long been viewed as the “responsible” route. But for property managers who need fast funding, this route can feel more like a maze than a solution.

The Bank Loan Experience:

- Endless paperwork — tax returns, business plans, property appraisals

- Strict credit score requirements — often above 680

- Collateral demands — property titles, liens, or personal guarantees

- Slow turnaround times — 30 to 90+ days just to get approved

- Limited flexibility — funds often restricted to specific use cases like purchasing, not renovating or maintenance

Let’s say a multi-unit property experiences a plumbing issue affecting half the building. Waiting 60 days for a loan approval is not an option—you’ll lose tenants and income.

According to the National Small Business Association, 68% of small business owners report difficulty obtaining traditional financing. And in the real estate sector, banks are even more cautious—especially if your portfolio includes multiple mortgages or older properties.

For many property managers, this slow, inflexible process just doesn’t work anymore.

III. What Is a Merchant Cash Advance—and Why It Works for Property Managers

Enter the Merchant Cash Advance (MCA)—a funding solution that aligns with how real estate businesses actually operate.

What is an MCA?

A Merchant Cash Advance is not a loan. It’s a purchase of your future receivables. In simple terms, a funder gives you fast capital now in exchange for a percentage of your future income (like rent payments).

Why It Works for Property Managers:

- Speed: Most MCAs fund within 24 to 72 hours

- No collateral required: You don’t risk your properties or assets

- Low credit requirements: Approvals are based on cash flow, not credit score

- Flexible use: Use funds for repairs, renovations, legal costs, tax payments, or expansion

- Tailored repayments: Based on daily or weekly revenue, not fixed monthly payments

Example:

“James, a landlord in Dallas, had a 12-unit property where the roof caved in after a storm. Insurance would take 90 days to pay. His bank offered a loan—but only after a new appraisal and two months of waiting. Instead, James secured a $35,000 MCA and began repairs within 48 hours. His tenants stayed, rent continued flowing, and he avoided months of lost income.”

This kind of speed and adaptability is why MCAs are a natural fit for the real estate industry.

IV. MCA vs. Bank Loan: Side-by-Side Comparison Table

Here’s how the two stack up:

| Feature | Traditional Bank Loan | Merchant Cash Advance (MCA) |

|---|---|---|

| Funding Speed | 30–90 days | 24–72 hours |

| Credit Score Dependence | High (typically 680+) | Low (based on revenue, not score) |

| Collateral Required | Often yes | No |

| Use of Funds | Restricted (purchase, capital only) | Flexible (repairs, payroll, taxes, etc.) |

| Approval Rate | ~20–30% for small businesses | ~70–90% |

| Repayment | Fixed monthly payments | Variable, based on daily/weekly cash flow |

| Risk of Asset Loss | High (default could trigger foreclosure) | None (no liens or property at risk) |

This comparison speaks for itself—for property managers who need working capital quickly, MCAs offer a clear advantage.

V. Use Cases: How Real Estate Businesses Use MCA Funds

One of the key advantages of a Merchant Cash Advance is its versatility. Here are some real-world scenarios where property managers and real estate investors benefit from MCA funding:

1. Emergency Repairs

A broken water main, mold outbreak, or collapsed ceiling can’t wait 30 days. An MCA provides immediate funds to address emergencies and maintain tenant satisfaction.

2. Unit Renovations Between Tenants

Want to increase rent by 20%? Upgrade appliances, repaint, and modernize your units with MCA funds to justify higher prices—and improve ROI.

3. Covering Seasonal Vacancies

In vacation towns or student housing, seasonal dips are common. An MCA bridges the gap between high-occupancy months, so you stay financially stable year-round.

4. Expanding Your Portfolio

Spot a great deal on a new property but need capital fast for inspection fees, contractor down payments, or permits? MCA gives you the liquidity to seize the opportunity.

5. Handling Legal or Tax Expenses

Sudden property tax increases or legal disputes with tenants can be a cash drain. Use MCA funds to stay on top of legal obligations without dipping into reserves.

Real Example:

“A New Jersey property manager used a $60,000 MCA to renovate four outdated apartments. Within two months, each unit was leased at a 25% rent increase. The MCA paid itself off within 6 months through new tenant revenue.”

VI. Addressing the Critics: Is an MCA Too Expensive?

Critics often claim that MCAs are expensive—and it’s true that the cost structure is different than traditional loans.

Let’s Break It Down:

- MCAs use a factor rate, not an interest rate. A factor rate of 1.3 on a $20,000 advance means you repay $26,000.

- There’s no compounding interest, but the repayment is typically faster (6–12 months).

The Trade-Off: Speed and Opportunity

Yes, the cost may be higher on paper—but the value is in the speed and opportunity:

- Avoid losing tenants due to delayed repairs

- Capture investment deals that won’t last

- Complete renovations now, charge higher rent tomorrow

Would you rather wait 90 days for a cheaper loan—or pay slightly more and solve the problem this week?

ROI > APR

If MCA funds let you increase your property income by 20%, the math often works in your favor.

VII. Choosing the Right MCA Provider for Real Estate Needs

Not all MCAs are created equal. If you’re considering this path, choose a provider who understands the unique needs of property managers.

What to Look For:

- Real estate experience – Ask for case studies or examples

- No hidden fees – Transparent repayment terms

- Fast approvals – Most funders can pre-approve in 24 hours

- Tailored support – Look for personalized funding strategies

Pro Tip:

Prepare these documents to speed up approval:

- 3–6 months of business bank statements

- Rent roll or property income statements

- Contractor estimates (if using funds for renovation)

- Tax ID or business license

Working with a trusted provider like Smart Business Funding can ensure a smooth process and reliable funding.

VIII. Final Verdict: Why More Property Managers Are Making the Switch

The real estate market doesn’t wait—and neither should you. Property managers are realizing that fast, flexible funding is essential for keeping operations smooth, tenants happy, and properties profitable.

Bank loans come with baggage: delays, restrictions, and denials.

Merchant Cash Advances offer freedom.

They empower you to:

- Act fast when opportunity strikes

- Handle emergencies without financial stress

- Grow your business without giving up equity or waiting on banks

So if you’re tired of long waits and rigid rules, you’re not alone. Thousands of property managers are dumping bank loans—and thriving with MCAs.

IX. FAQ: Real Estate + MCA Quick Questions

Q: Can I use an MCA to pay contractors or renovation crews?

Absolutely. MCA funds are unrestricted—use them for labor, materials, or even permits.

Q: What if my credit score is low?

MCA providers focus on your monthly revenue, not your credit history.

Q: Will an MCA put a lien on my property?

No. Unlike bank loans, MCAs are unsecured and do not require collateral.

Q: How fast can I get funding?

Most property managers get funded within 24–72 hours after approval.

X. Ready to Fund Smarter, Not Slower?

Still relying on slow, outdated funding from the bank? It’s time to explore what alternative real estate financing can do for your business.

✅ No collateral required

✅ Approvals within hours

✅ Cash in your account this week