Which Alternative Funding Works Best for Restaurants, Retail, and Service Businesses?

By a Business Owner, for Business Owners

Why Industry-Specific Funding Choices Matter in 2025

In business, one-size-fits-all rarely works—especially when it comes to funding. Restaurants, retail shops, and service providers don’t just differ in what they sell; they also differ in cash flow patterns, expenses, and revenue cycles.

A restaurant may need funding fast to replace a broken freezer before the dinner rush. A retail store might need extra working capital to stock up for the holiday season. A service business could require investment in new tools or a marketing campaign to attract high-value clients.

And in 2025, the shift away from traditional bank loans is more pronounced than ever. Why?

- Banks take too long — weeks or even months for approval.

- Credit requirements are rigid, shutting out business owners with less-than-perfect scores.

- Collateral demands don’t align with many modern businesses.

That’s where alternative business funding steps in: faster, more flexible, and tailored to industries with unique needs.

Understanding the Alternative Funding Landscape

Alternative funding refers to any type of business financing that isn’t a traditional bank loan. It exists to bridge the gap between what banks offer and what small businesses actually need.

Here are the most common forms:

Merchant Cash Advance (MCA)

You receive a lump sum in exchange for a percentage of your future sales. Repayments happen daily or weekly based on actual sales performance.

Why it works for many industries:

- Fast approval (often within 24–48 hours)

- Flexible repayments that scale with sales

- Accessible to businesses with fair or even poor credit

Revenue-Based Financing

You receive capital in exchange for a percentage of your monthly revenue until the agreed amount is repaid.

Why it’s a good fit:

- Lower payments in slow months

- No fixed due date—repayment tied to performance

- Works well for growth-oriented businesses

Crowdfunding

Raising small amounts of money from many people—through reward-based, donation-based, or equity-based campaigns.

Why it can help:

- Generates marketing buzz while raising funds

- No repayment required for reward/donation-based campaigns

- Community-driven support

Equipment Financing Alternatives

Funding specifically for purchasing or upgrading equipment without going through traditional bank loans.

Why it’s useful:

- Often easier to qualify for since equipment serves as collateral

- Preserves working capital for other expenses

Invoice Factoring

Selling your unpaid invoices to a factoring company for immediate cash.

Why it makes sense for some businesses:

- Unlocks money tied up in accounts receivable

- Ideal for B2B businesses with slow-paying clients

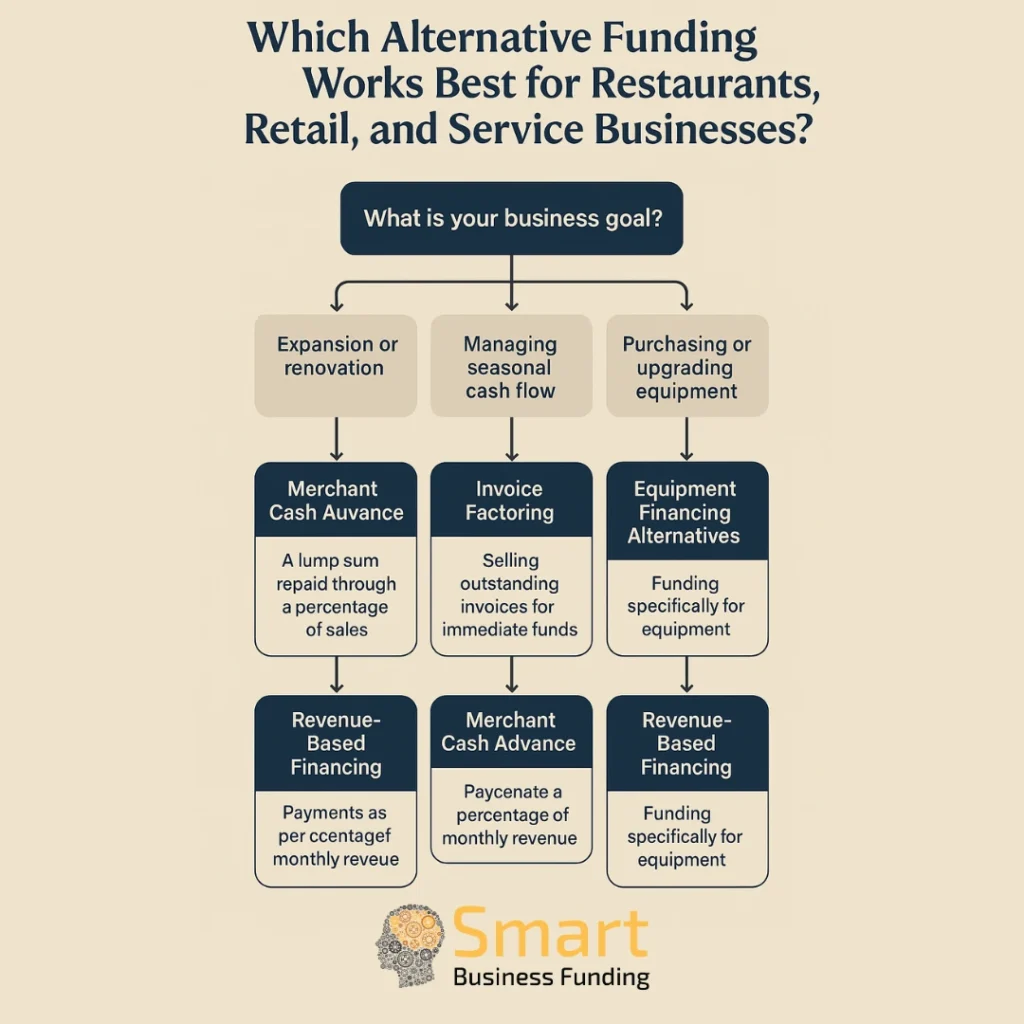

Best Alternative Funding for Restaurants

Common Funding Needs for Restaurants

Restaurants operate on tight margins and rely heavily on speed. Funding needs often arise suddenly, such as:

- Expansion and renovations — Adding seating, revamping decor, or opening a new location

- Seasonal cash flow challenges — Slow months after holiday rushes or seasonal tourism dips

- Marketing and promotions — Special events, loyalty programs, or ad campaigns

- Equipment repair or upgrades — From ovens to walk-in freezers, downtime means lost revenue

Top Funding Options for Restaurants

1. Merchant Cash Advance (MCA)

Best for: Emergency repairs, quick expansion, or seasonal marketing boosts

- Fast access to capital, sometimes within 24 hours

- Repayments automatically adjust with daily sales

- No collateral required

2. Revenue-Based Financing

Best for: Growth-oriented restaurants expanding menus or adding locations

- Payments scale with revenue, easing pressure in slow weeks

- Encourages reinvestment into marketing and staffing during growth

3. Equipment Financing Alternatives

Best for: Kitchen equipment upgrades or replacements

- Protects cash flow while acquiring essential tools

- Often easier approval because the equipment serves as collateral

Pros and Cons for Restaurants

Pros:

- Flexible repayment options that match sales cycles

- Fast funding keeps downtime minimal

- Works even with moderate credit

Cons:

- MCAs can have higher costs

- Overreliance on short-term funding can strain future cash flow

Best Alternative Funding for Retail Businesses

Common Funding Needs for Retail

Retail has its own rhythm—inventory cycles, seasonal peaks, and consumer trends can all affect cash flow. Common funding needs include:

- Inventory stocking — Especially before peak seasons like holidays or back-to-school

- Store renovations or rebranding — Staying competitive in visual appeal and experience

- Expanding to e-commerce — Website development, online marketing, and logistics

Top Funding Options for Retail

1. Merchant Cash Advance (MCA)

Best for: Stocking inventory before sales peaks

- Provides quick working capital to take advantage of supplier discounts

- Repayments align with daily or weekly sales volume

2. Invoice Factoring

Best for: Retailers with wholesale or B2B customers

- Turns unpaid invoices into immediate working capital

- Eliminates waiting 30–90 days for payments

3. Crowdfunding

Best for: Launching new products or branding campaigns

- Generates hype before a product hits the shelves

- Builds a loyal community of early adopters

Pros and Cons for Retail

Pros:

- Access capital quickly to seize seasonal opportunities

- Flexible repayment reduces stress during slow months

- Crowdfunding doubles as a marketing strategy

Cons:

- Some options can be costly if not timed correctly with sales cycles

- Crowdfunding requires heavy promotion to succeed

Best Alternative Funding for Service Businesses

Common Funding Needs for Service-Based Businesses

Unlike restaurants and retail, service-based businesses often have fewer tangible assets but still face big expenses:

- Marketing campaigns — To attract new clients or expand into new markets

- Hiring and training staff — Especially for skilled trades or specialized services

- Upgrading tools and technology — Staying competitive with the latest equipment or software

Top Funding Options for Service Businesses

1. Merchant Cash Advance (MCA)

Best for: Covering payroll, marketing costs, or unexpected expenses

- Quick funding to keep projects moving

- Works even for businesses with uneven income cycles

2. Revenue-Based Financing

Best for: Project-based businesses with predictable but fluctuating revenue

- Payments adjust to match contract completions or client payments

- Encourages growth without overextending

3. Equipment Financing Alternatives

Best for: Trades and specialized services

- Affordable way to acquire tools without draining reserves

- Equipment acts as collateral, easing approval

Pros and Cons for Service Businesses

Pros:

- Funding options that adapt to uneven revenue streams

- Allows investment in growth without heavy upfront costs

- Works for businesses with limited physical assets

Cons:

- May be harder to secure large amounts without strong revenue history

- Overestimating future sales can cause repayment strain

Comparing Funding Options Across Industries

| Funding Type | Speed | Flexibility | Best For Restaurants | Best For Retail | Best For Services |

|---|---|---|---|---|---|

| Merchant Cash Advance (MCA) | 24–48 hrs | High | Emergency repairs, seasonal boosts | Inventory stocking | Payroll, marketing |

| Revenue-Based Financing | 3–7 days | High | Expansion, growth projects | Online expansion | Project-based income |

| Crowdfunding | Months | Medium | New menu launches | Product launches | Service packages |

| Equipment Financing | 3–10 days | Medium | Kitchen upgrades | POS systems | Trade tools |

| Invoice Factoring | 1–3 days | Medium | N/A | B2B retail invoices | B2B service invoices |

Mistakes to Avoid When Choosing Alternative Funding

- Choosing based on speed alone — Fast isn’t always financially healthy.

- Ignoring repayment terms — Always calculate total payback, not just the advance amount.

- Using one funding type for every problem — Match the solution to the goal.

- Overestimating seasonal sales — Leads to cash flow crunch when repayments hit.

Trends to Watch for in 2025

- Industry-specific MCA packages — Tailored repayment terms for restaurants, retail, and service sectors.

- AI-driven approvals — Faster underwriting with better risk matching.

- Hybrid funding models — Combining short-term cash (MCA) with longer-term lines of credit.

- More flexible repayment terms — Allowing seasonal adjustments for peak/off-peak industries.

Conclusion – Matching Funding to Your Industry Needs

The best alternative funding in 2025 isn’t about chasing the lowest rate or the fastest approval—it’s about finding the right fit for your industry, your goals, and your cash flow cycle.

- Restaurants benefit from speed and flexibility—MCA and revenue-based financing lead the pack.

- Retail businesses thrive when they can align funding with inventory cycles—MCA, crowdfunding, and invoice factoring shine here.

- Service businesses need adaptable repayment structures—revenue-based financing and equipment alternatives are often the best match.

Choose funding that empowers your business today without compromising tomorrow.

Ready to get the perfect funding for your restaurant, retail store, or service business?

Contact Smart Business Funding today and secure a tailored solution in as little as 24 hours.