The Surprising History of Merchant Cash Advances (It Started with Credit Cards!)

How One Funding Innovation Grew from Retail Transactions into a Billion-Dollar Industry

🔹 The Billion-Dollar Secret Hiding in Plain Sight

What if one of the fastest-growing funding tools for small businesses started not in a bank, but in a credit card machine?

That’s the surprising origin story behind the Merchant Cash Advance (MCA)—a modern solution to an old problem: small businesses need capital, and banks aren’t always willing to help. Born from the rise of credit card transactions in the ’90s, MCAs quietly evolved from a niche product into a billion-dollar financial industry.

Today, in 2025, MCAs provide fast, flexible funding to thousands of businesses—from food trucks to freelancers—without the red tape of traditional loans. But to understand why they work so well, we need to understand where they came from.

🔹 What Is a Merchant Cash Advance—Really?

A Merchant Cash Advance is not a loan. Instead, it’s a purchase of your future revenue. A funding provider gives your business a lump sum of cash upfront in exchange for a portion of your future daily sales. Repayment is made automatically through a percentage of your credit card or bank deposits.

This structure means no fixed payments, no collateral, and no waiting weeks for bank approval. Instead, funding can happen in 24–48 hours.

Why it’s better than a traditional loan:

Bank loans involve lengthy applications, credit score scrutiny, and strict monthly payments. MCAs offer a revenue-based model—you repay more on busy days and less on slow ones. It’s the perfect fit for businesses with seasonal or fluctuating cash flow.

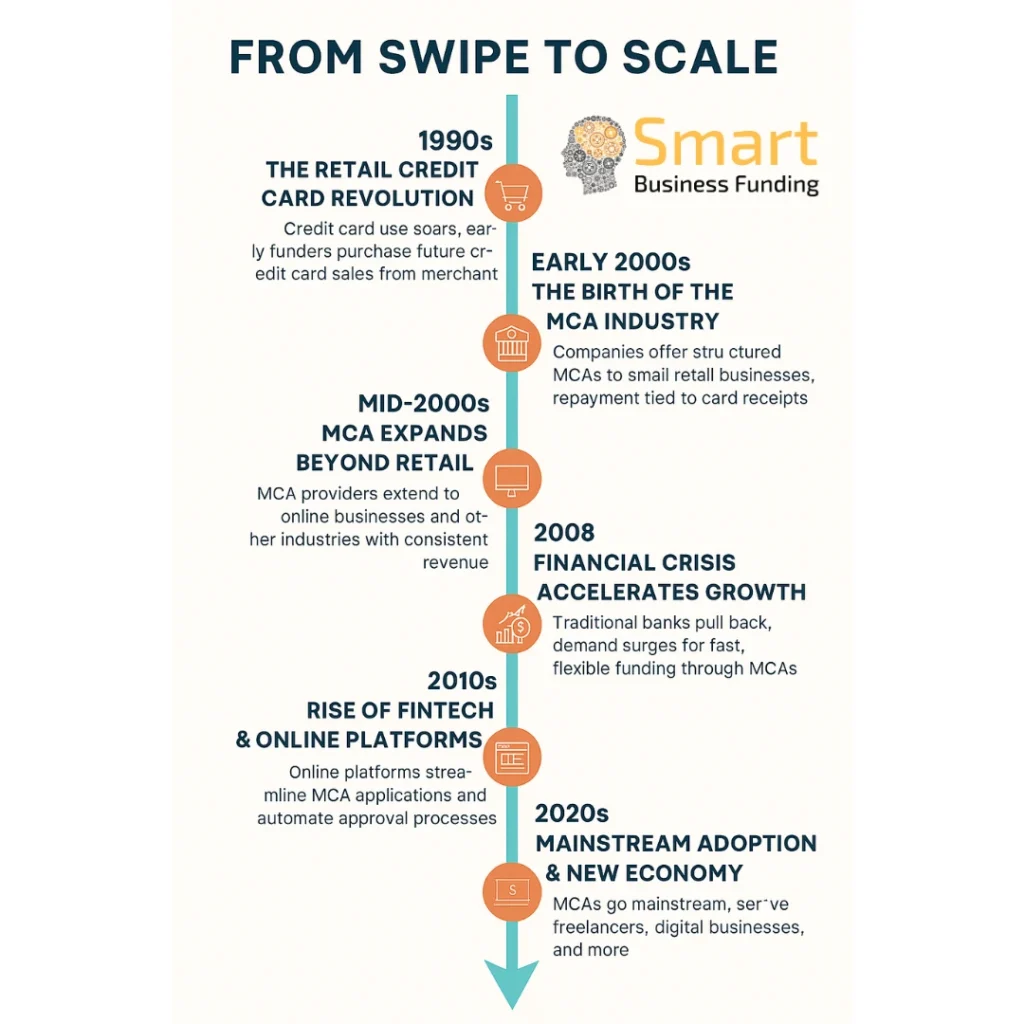

🔹 1990s – The Retail Credit Card Revolution

During the 1990s, the U.S. economy saw a dramatic rise in credit card usage. As consumers swiped more at checkout, small businesses began seeing large portions of their income arrive through Visa and Mastercard transactions.

At the same time, these same businesses struggled to get bank loans. High interest rates, strict collateral requirements, and skepticism toward small or minority-owned businesses kept traditional capital out of reach.

This gap opened a window for early funders: What if you could buy a percentage of a business’s future credit card sales in exchange for cash today?

That was the seed that grew into the modern MCA.

Why it’s better than a traditional loan:

Instead of judging a business by its assets or credit score, early MCA providers judged it by one thing: daily income. If customers were swiping cards, that business was fundable—even if no bank agreed.

🔹 Early 2000s – The Birth of the MCA Industry

By the early 2000s, that idea evolved into a structured product. A handful of private companies began offering formal Merchant Cash Advances to small retail businesses—especially restaurants, nail salons, gas stations, and convenience stores.

These providers installed card-reading software that would automatically deduct a fixed percentage of daily credit card receipts to repay the advance. It was seamless, flexible, and scalable.

The model grew fast, particularly in urban areas where banks were absent or unwilling to take risks.

Why it’s better than a traditional loan:

Unlike banks, these funders didn’t require business plans, years of tax returns, or perfect credit. The business’s card sales spoke for themselves, and funding was based on real-time performance—not paper projections.

🔹 Mid-2000s – MCA Expands Beyond Retail

With the rise of ecommerce and digital payments in the mid-2000s, MCA providers realized that funding didn’t have to stop at brick-and-mortar shops.

Businesses accepting payments through online processors like PayPal, Square, or Stripe could also be funded. The MCA model shifted from just “merchant” (point-of-sale) to any business with consistent revenue.

As a result, freelancers, consultants, and online sellers began qualifying for MCAs—even if banks wouldn’t touch them.

Why it’s better than a traditional loan:

This expansion proved that MCA wasn’t limited to any one industry. As long as you had predictable income—online or offline—you could get funded quickly, without waiting months for a bank’s approval committee.

🔹 2008 Financial Crisis – The Turning Point

When the 2008 financial crisis hit, traditional lending dried up overnight. Banks pulled back sharply from small business lending, leaving millions of entrepreneurs stranded.

But MCAs? They surged. As businesses faced tighter cash flow, many turned to the speed and simplicity of Merchant Cash Advances to stay afloat. MCA providers saw record growth during this time.

The recession became a defining moment, proving that MCAs could survive—and thrive—when banks couldn’t.

Why it’s better than a traditional loan:

In a crisis, speed matters. MCA providers often deliver funding within 1–2 days, compared to the weeks or months banks require. That agility helped thousands of businesses survive the downturn—and kept employees paid.

🔹 2010s – The Rise of Fintech & Online MCA Platforms

The next evolution came with fintech. Automation, digital banking, and real-time data enabled MCA platforms to streamline the application and approval process even further.

Instead of submitting piles of paperwork, businesses could now upload bank statements online and receive offers the same day. Companies like Smart Business Funding led the way in offering user-friendly, transparent, and tech-enabled funding solutions.

As a result, MCA became a mainstream alternative to loans, not just a last resort.

Why it’s better than a traditional loan:

Modern MCA platforms integrate directly with business accounts, removing guesswork and speeding up decisions. Meanwhile, banks still rely on outdated manual processes and hard-credit pulls. MCA is built for the digital age.

🔹 2020s – MCAs Go Mainstream in the Gig and Creator Economy

The 2020s brought a major shift in the labor force. From content creators and Uber drivers to TikTok shops and Etsy entrepreneurs, the economy exploded with non-traditional income streams.

These businesses often lack formal documentation, credit history, or W2s—but they’re still generating revenue. MCA providers adapted again, now offering ACH-based repayment models that draw from bank deposits, not just card sales.

This flexibility made MCAs a perfect fit for modern entrepreneurs.

Why it’s better than a traditional loan:

Banks haven’t caught up to the creator economy. Most still ask for outdated metrics. MCAs use live data to approve gig workers, freelancers, and digital-first businesses based on performance—not paperwork.

🔹 Why MCA Grew While Traditional Loans Shrunk

While MCAs expanded across industries and platforms, traditional bank loans shrank—especially for startups, minority-owned businesses, and those with low credit.

Banks rely on conservative models. They say no to risk. MCA providers, on the other hand, say: “Show me your revenue—and let’s move.”

That’s why MCAs now fund billions annually—from restaurants and salons to consultants and construction crews.

| Merchant Cash Advance | Traditional Business Loan |

|---|---|

| Revenue-based approvals | Credit score & collateral required |

| Approval in 24–48 hours | Weeks or months of processing |

| Flexible daily or weekly repayment | Fixed monthly payments |

| No collateral or hard credit pull | Often requires personal guarantee |

| Works for any industry | Only “safe” or conventional sectors |

🔹 The Role of Smart Business Funding in Modern MCA Evolution

As the industry matured, Smart Business Funding emerged as a trusted MCA provider for today’s small businesses.

With a focus on speed, simplicity, and support, Smart Business Funding helps entrepreneurs:

- Apply online in minutes

- Get decisions within hours

- Receive cash in as little as 24 hours

Whether you’re a bakery, a barber, or a boutique ecommerce seller, Smart Business Funding offers non-judgmental, fast, and flexible working capital when banks say no.

From Card Swipes to Capital—The MCA Journey

From humble beginnings tied to credit card machines in the 1990s, Merchant Cash Advances have grown into one of the most powerful tools in modern small business finance.

They’ve adapted to recessions, technological revolutions, and even the creator economy—proving that flexible, fast funding beats slow bureaucracy every time.

If your business needs working capital and doesn’t fit the mold, it’s time to consider the funding method that was made for real-world entrepreneurs—not just perfect borrowers.

👉 Ready to find out how much you qualify for?

Smart Business Funding is here to help you fund your next step—without the bank runaround. Apply today and get approved in just 24–48 hours.