The Business Owner’s Guide to Choosing the Best Alternative Funding in 2025

By a Business Owner, for Business Owners

Why Alternative Business Funding Matters More Than Ever in 2025

If you’ve run a business for more than five minutes, you know cash flow can make or break you. One big order, a late-paying client, a broken piece of equipment—suddenly you’re scrambling for working capital.

For decades, the standard advice was: “Go to the bank.” But in 2025, that advice feels outdated for many small business owners. Traditional loans are often slow, require perfect credit, and can take weeks—sometimes months—to process. And if you’ve ever been through a loan application only to get denied after all that waiting… well, you know how frustrating it is.

That’s why alternative business funding has exploded. From merchant cash advances (MCAs) to crowdfunding, non-bank funding is giving entrepreneurs the speed, flexibility, and accessibility they need. According to industry data, more than 40% of small businesses now use some form of alternative financing—and that number is climbing.

In this guide, I’ll walk you through exactly how to choose the best alternative funding in 2025, based on your goals, financial position, and business model—straight from a business owner’s perspective.

Understanding Alternative Funding—A Quick Overview

Alternative funding is any source of business capital that doesn’t come from a traditional bank loan. It exists to fill the gaps banks can’t—or won’t—fill.

Here are the most common types:

1. Merchant Cash Advance (MCA)

You get a lump sum in exchange for a percentage of your future sales. Repayments happen automatically through your daily or weekly transactions.

Best for: Businesses with steady sales, retail, restaurants, service industries.

Why business owners like it: Fast approval, bad credit friendly, no collateral.

2. Revenue-Based Financing

You receive funding and repay as a fixed percentage of your monthly revenue until the agreed amount is paid back.

Best for: Growing businesses with fluctuating income.

Why business owners like it: Payments scale with revenue—lower in slow months, higher in busy months.

3. Crowdfunding

You raise small amounts of money from a large number of people, typically online. This can be reward-based, donation-based, or equity-based.

Best for: New product launches, creative projects, community-based businesses.

Why business owners like it: Builds brand awareness while raising funds.

4. Peer-to-Peer Lending

Individual investors lend to you via an online platform, bypassing banks.

Best for: Businesses that want a personal, flexible funding approach.

Why business owners like it: Can be quicker and more accessible than traditional lending.

5. Equipment Financing Alternatives

Funding specifically for purchasing or upgrading equipment, without a standard bank loan.

Best for: Construction, manufacturing, medical, auto repair, or any equipment-heavy industry.

Why business owners like it: Assets often serve as collateral, making approval easier.

6. Invoice Factoring

You sell your unpaid invoices to a factoring company for immediate cash, minus a fee.

Best for: Businesses with slow-paying customers but strong invoice volume.

Why business owners like it: Unlocks cash tied up in accounts receivable quickly.

How to Choose the Right Alternative Funding for Your Business

Choosing the best alternative funding option isn’t just about who says “yes” first—it’s about aligning the funding with your goals, financial health, and industry reality.

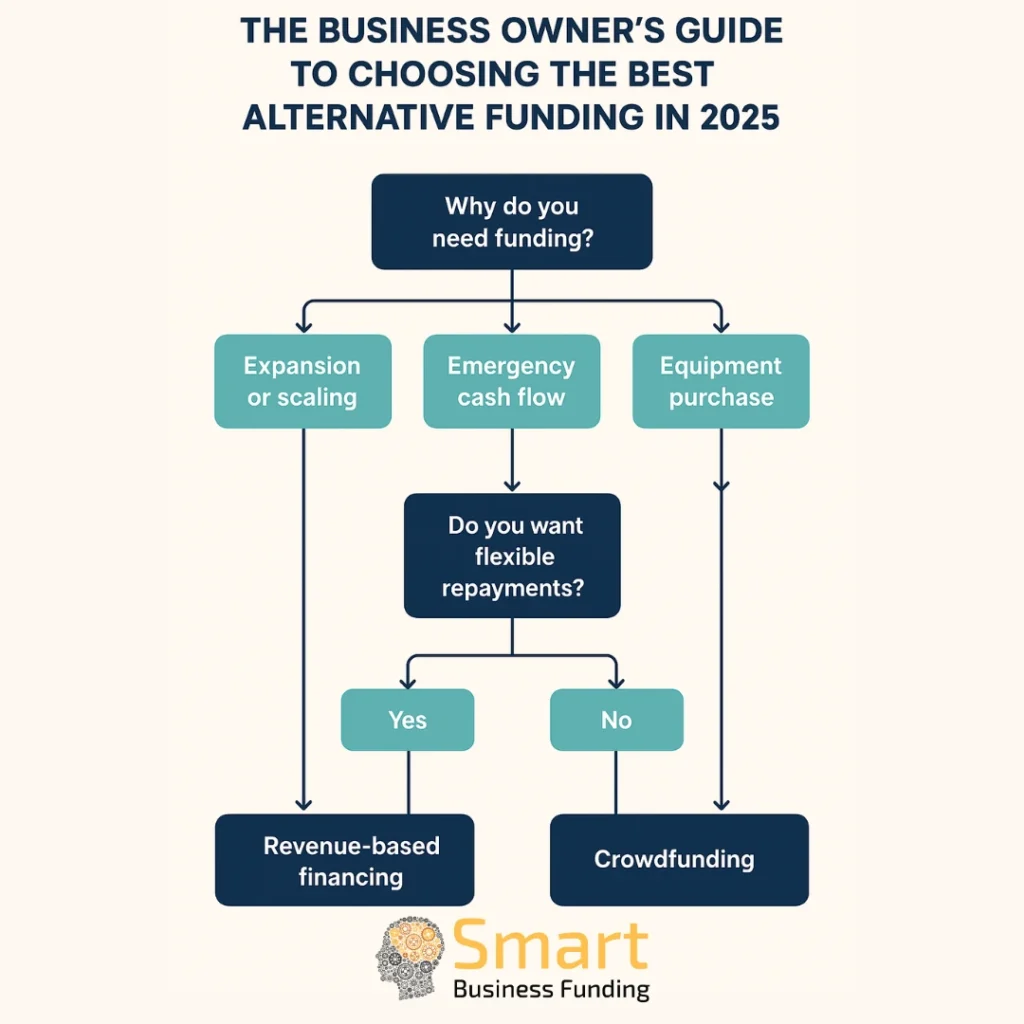

Step 1 – Define Your Business Goals

Ask yourself: Why do I need this funding?

- Expansion: Opening a new location, adding staff, scaling operations.

- Emergency Cash Flow: Covering payroll, paying suppliers, keeping the lights on.

- Equipment Purchase: Upgrading tools or machinery.

- Marketing Push: Funding a campaign that can increase revenue.

Your goal will guide you toward the right funding type.

Step 2 – Understand Your Financial Position

- Credit Score: Many alternative options are credit-flexible, but some require a minimum score.

- Monthly Revenue: The higher your consistent revenue, the more options open to you.

- Seasonality: Seasonal businesses should favor repayment structures that flex with income.

Step 3 – Compare Speed, Flexibility, and Cost

Think of it as a triangle—you often get two of these three, but rarely all three at once:

- Speed: MCA and invoice factoring are the fastest (often 24–48 hours).

- Flexibility: Revenue-based financing adjusts to your cash flow.

- Cost: Crowdfunding can be the cheapest if reward-based, but takes time.

Step 4 – Consider Industry Fit

Different industries naturally align with certain funding types:

- Retail/Restaurants: MCAs and revenue-based financing.

- Construction/Manufacturing: Equipment financing alternatives.

- Creative/Tech Startups: Crowdfunding or equity-based funding.

- Service Businesses: MCA or invoice factoring.

The Pros and Cons of Popular Alternative Funding Options

Let’s break down the major funding types from a real-world perspective:

Merchant Cash Advance (MCA)

Pros:

- Fast approval (often under 48 hours)

- Flexible repayment tied to sales

- Works with lower credit scores

Cons:

- Higher cost than traditional loans

- Daily/weekly repayment can pinch low-margin businesses

Revenue-Based Financing

Pros:

- Payments match your revenue performance

- No fixed monthly obligation

- Encourages sustainable growth

Cons:

- Takes longer to repay during slow seasons

- Not suitable for businesses with unpredictable sales

Crowdfunding

Pros:

- Builds brand awareness

- No repayment for reward/donation-based campaigns

- Can validate your business idea

Cons:

- Requires strong marketing effort

- Can take months to fund successfully

Equipment Financing Alternatives

Pros:

- Asset-backed funding increases approval odds

- Keeps cash free for other needs

Cons:

- Risk of equipment repossession

- Limited to equipment-related purchases

Invoice Factoring

Pros:

- Turns unpaid invoices into immediate cash

- No debt incurred

Cons:

- Reduces overall profit margin

- Customers may be contacted by factoring company

How to Match Funding to Your Business Goals

Here’s a quick cheat sheet:

- Expansion & Scaling: MCA or revenue-based financing

- Seasonal Cash Flow Issues: MCA or invoice factoring

- New Product Launch: Crowdfunding or MCA

- Equipment Upgrades: Equipment financing alternatives

- Bad Credit Needs: MCA or revenue-based financing

Mistakes Business Owners Make When Choosing Alternative Funding

- Focusing Only on Speed – Fast money can be expensive money.

- Ignoring Repayment Terms – Look at the total payback, not just the advance.

- Choosing the Wrong Tool for the Job – Funding type must match your use case.

- Over-Borrowing – Taking more than you need can lead to repayment strain.

2025 Funding Trends Every Business Owner Should Watch

- AI-Powered Approvals – Automated underwriting is making funding decisions faster.

- Hybrid Funding Models – Combinations like MCA + line of credit are becoming popular.

- Decline in Bank Loan Dependence – Small businesses are increasingly bypassing banks entirely.

Conclusion – Your Funding, Your Future

The best alternative funding option in 2025 depends on you: your goals, your cash flow, your industry, and your tolerance for repayment terms.

Whether it’s the speed of an MCA, the flexibility of revenue-based financing, or the brand boost of crowdfunding, the right choice will empower—not burden—your business.

Ready to explore your perfect funding fit?

Contact Smart Business Funding today and get matched with a solution tailored to your goals—in as little as 24 hours.