Merchant Cash Advance vs. Traditional Loans in 2026: Pros & Cons for Small Businesses

As 2026 begins, small business owners are facing a familiar question with a new level of urgency: How do I fund growth without putting my business at risk? Rising costs, tighter bank requirements, and fast-moving market opportunities mean choosing the right funding option matters more than ever.

Two of the most common choices remain Merchant Cash Advances (MCAs) and traditional business loans—but they work very differently. Understanding their pros, cons, and ideal use cases can help you make a smarter funding decision in 2026.

In this guide, we break down Merchant Cash Advance vs. Traditional Loans, so you can decide which option best supports your cash flow, goals, and growth plans this year.

Why Funding Choices Matter More in 2026

The funding landscape has shifted significantly over the last few years. Many small businesses are operating in an environment of:

- Higher operating costs

- Slower customer payments

- Increased demand for flexibility

- Stricter bank underwriting standards

At the same time, opportunities haven’t slowed down. Businesses still need capital for inventory, marketing, equipment, payroll, and expansion—often on short notice.

That’s why alternative financing options like merchant cash advances continue to grow in popularity alongside traditional loans.

What Is a Merchant Cash Advance (MCA)?

A Merchant Cash Advance is not a loan in the traditional sense. Instead, a funding company provides your business with a lump sum of capital in exchange for a percentage of your future sales.

Repayment happens automatically—typically daily or weekly—based on your revenue.

How MCAs Work

- You receive funding quickly (often within 24–48 hours)

- Repayments adjust with your sales volume

- Approval focuses more on cash flow than credit score

MCAs are commonly used by businesses that need fast working capital and don’t want to wait weeks—or months—for a bank decision.

What Is a Traditional Business Loan?

A traditional business loan is a fixed-term loan offered by banks or credit unions. You borrow a specific amount and repay it over time with interest through fixed monthly payments.

How Traditional Loans Work

- Longer approval and funding timelines

- Fixed repayment schedule

- Often requires strong credit, collateral, and financial history

While traditional loans can be cost-effective, they aren’t always accessible or practical for every small business—especially those that need capital quickly.

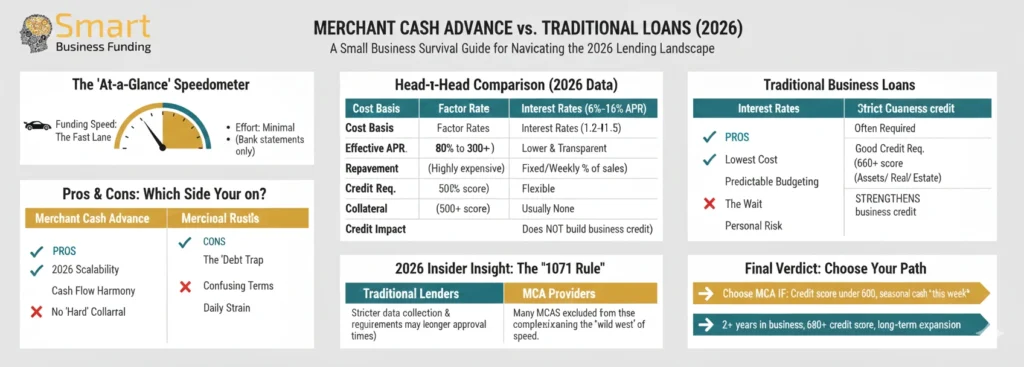

Merchant Cash Advance vs. Traditional Loans: Key Differences

1. Speed of Funding

Merchant Cash Advance

- Approval can happen in hours

- Funding often arrives within 1–2 business days

- Ideal for urgent cash flow needs

Traditional Loans

- Application and underwriting can take weeks

- Funding delays may cause missed opportunities

Winner for speed: Merchant Cash Advance

2. Approval Requirements

Merchant Cash Advance

- Focus on business revenue and cash flow

- Credit score requirements are more flexible

- Often available to newer businesses

Traditional Loans

- Strong credit score required

- Financial statements, tax returns, and collateral often needed

- Strict underwriting standards

Winner for accessibility: Merchant Cash Advance

3. Repayment Structure

Merchant Cash Advance

- Repayment fluctuates with sales

- Payments are typically daily or weekly

- Easier to manage during slower sales periods

Traditional Loans

- Fixed monthly payments regardless of revenue

- Can strain cash flow during slow seasons

Winner for cash flow flexibility: Merchant Cash Advance

4. Cost & Transparency

Merchant Cash Advance

- Uses factor rates instead of interest

- Can be more expensive over time

- Best for short-term funding needs

Traditional Loans

- Lower interest rates

- Predictable long-term cost

- Better for large, long-term investments

Winner for lower cost: Traditional Loans

5. Best Use Cases

Merchant Cash Advances are ideal for:

- Inventory purchases

- Marketing campaigns

- Covering payroll gaps

- Emergency expenses

- Seasonal sales spikes

Traditional Loans are ideal for:

- Long-term expansion

- Real estate or large equipment

- Businesses with strong financial profiles

- Predictable revenue streams

Pros & Cons Summary Table

Merchant Cash Advance

Pros

- Fast approval and funding

- Flexible repayment

- Easier qualification

- No fixed monthly payment

Cons

- Higher overall cost

- Frequent repayments

- Not ideal for long-term financing

Traditional Business Loans

Pros

- Lower interest rates

- Fixed repayment schedule

- Suitable for long-term investments

Cons

- Slow approval process

- Strict credit requirements

- Less flexibility during slow sales

Which Is Better for Small Businesses in 2026?

There’s no one-size-fits-all answer.

In 2026, many small businesses are choosing speed and flexibility over rigid financing, especially in fast-changing markets. That’s why merchant cash advances remain a powerful tool—when used strategically.

If your business:

- Needs capital quickly

- Has strong daily or weekly sales

- Wants repayment tied to revenue

An MCA may be the right choice.

If your business:

- Has excellent credit

- Can wait for approval

- Needs long-term, lower-cost funding

A traditional loan might make more sense.

How Smart Business Funder Helps Small Businesses Make the Right Choice

Smart Business Funder works with small business owners to evaluate funding options based on real cash flow needs—not just credit scores.

Instead of pushing a one-size-fits-all solution, Smart Business Funder helps businesses:

- Access fast working capital

- Understand funding terms clearly

- Match the right financing option to their goals

- Avoid unnecessary financial strain

Whether you’re preparing for a strong first quarter or planning for year-long growth, having the right funding partner can make all the difference.

Final Thoughts: Choose Funding That Works for Your Business

In 2026, smart business owners aren’t just asking “Can I get funded?”

They’re asking “Will this funding help me grow sustainably?”

Both merchant cash advances and traditional loans have their place—but understanding the pros, cons, and timing of each is key.

Before committing to any funding, evaluate:

- Your cash flow

- Your urgency

- Your repayment comfort level

- Your long-term goals

When funding aligns with strategy, growth becomes far more achievable.