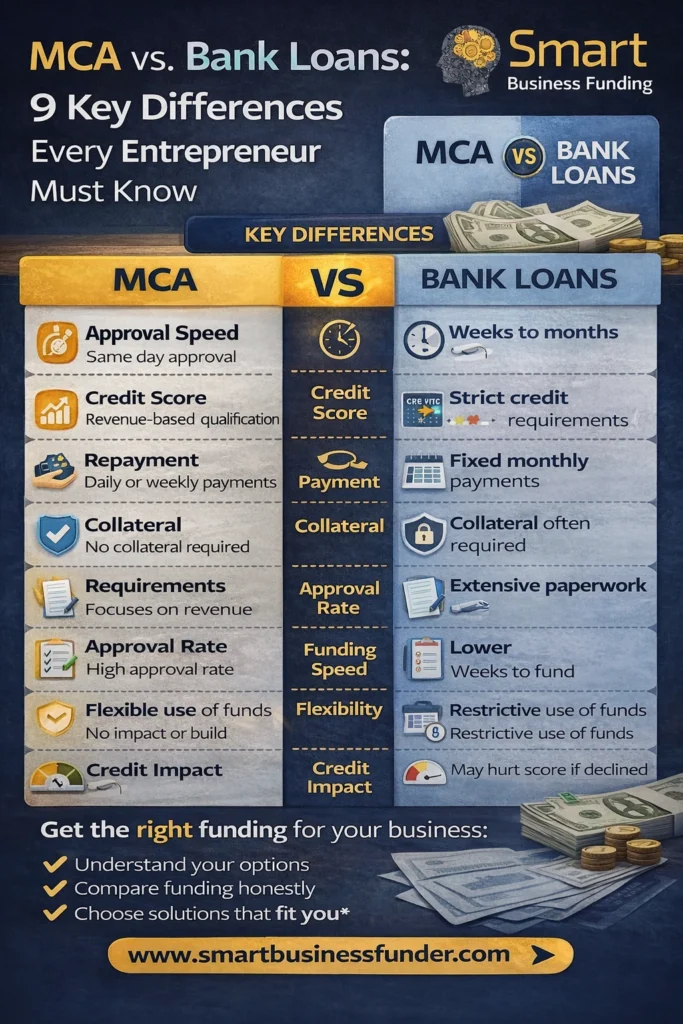

MCA vs. Bank Loans: 9 Key Differences Every Entrepreneur Must Know

When business owners start searching for funding, one of the most common questions in 2026 is:

Should I choose a Merchant Cash Advance (MCA) or a traditional bank loan?

Both options provide capital—but they are built for very different types of businesses, timelines, and cash-flow realities.

Below are 9 key differences every entrepreneur must understand before applying, so you can choose the option that actually supports your business growth.

1. Approval Speed

Bank Loans:

Approval can take weeks or months, with extensive underwriting and review.

MCA:

Approvals often happen same day, with funding in 24–48 hours.

Winner: MCA

Speed matters when opportunity or cash flow gaps appear.

2. Qualification Requirements

Bank Loans require:

- Strong personal and business credit

- Multiple years in business

- Tax returns and financial statements

MCA approvals are based on:

- Business revenue

- Cash flow consistency

- Time in business

Winner: MCA

Revenue matters more than credit score.

3. Credit Score Impact

Bank Loans:

Credit score plays a major role and denials can negatively impact future applications.

MCA:

Fair or poor credit is often acceptable because decisions focus on sales performance.

Winner: MCA

Ideal for growing businesses with imperfect credit.

4. Repayment Structure

Bank Loans:

- Fixed monthly payments

- Payments stay the same regardless of sales

MCA:

- Daily or weekly payments

- Payments fluctuate with revenue

Winner: Depends on cash flow

MCA offers flexibility when sales fluctuate.

5. Collateral Requirements

Bank Loans:

Often require collateral such as property, equipment, or personal guarantees.

MCA:

Typically no collateral required.

Winner: MCA

Less personal risk for business owners.

6. Paperwork & Documentation

Bank Loans:

- Extensive documentation

- Tax returns, financial statements, projections

MCA:

- Minimal paperwork

- Bank statements and application

Winner: MCA

Less time gathering documents, more time running your business.

7. Funding Use Restrictions

Bank Loans:

May limit how funds can be used.

MCA:

Funds can be used for:

- Payroll

- Inventory

- Marketing

- Equipment

- Expansion

Winner: MCA

Full flexibility to use capital where it’s needed most.

8. Time to Opportunity

Bank Loans:

Long timelines often mean missed opportunities.

MCA:

Designed for time-sensitive needs like:

- Inventory purchases

- Seasonal demand

- Growth opportunities

Winner: MCA

Fast capital keeps businesses competitive.

9. Best Use Case

Bank Loans are best for:

- Large, long-term investments

- Businesses with strong credit and time to wait

MCAs are best for:

- Growing businesses

- Short-term working capital

- Fast-moving opportunities

Winner: Depends on business needs

The right choice depends on your timeline and cash flow.

Why Many Entrepreneurs Choose MCA Funding in 2026

In today’s business environment, flexibility and speed often matter more than traditional lending structures.

That’s why many entrepreneurs turn to Merchant Cash Advances through experienced providers like Smart Business Funding—to secure funding that works with their business, not against it.

Smart Business Funding helps business owners:

✔ Understand their options

✔ Compare funding types honestly

✔ Choose solutions aligned with real cash flow

Final Thoughts: Choosing the Right Funding Matters

There’s no one-size-fits-all solution.

But understanding the differences between MCAs and bank loans helps you:

- Avoid delays

- Protect cash flow

- Choose funding that supports growth

The smartest funding decision is an informed one.