How Business Funding Is Structured in 2026 (Simple Breakdown)

Business funding in 2026 looks nothing like it did just a few years ago. Traditional loans are slower, approvals are tighter, and small businesses can’t afford to wait months for capital. At the same time, new funding models have evolved to prioritize speed, flexibility, and real cash-flow performance over perfect credit scores.

If you’re a business owner—or a broker trying to guide clients—this guide will walk you through exactly how business funding is structured in 2026, in simple, real-world terms.

No jargon. No fluff. Just how it actually works today.

The Big Shift: What Changed About Business Funding in 2026?

In 2026, lenders care less about:

- Your credit score

- Your tax returns

- Your personal net worth

And far more about:

- Your monthly revenue

- Your bank statement activity

- Your cash flow consistency

- Your ability to scale

Why? Because modern funding is built around performance-based risk, not old-school paperwork.

The 5 Main Business Funding Structures in 2026

Most business funding today falls into one of these five structures:

1. Merchant Cash Advances (MCAs)

What it is:

A business receives a lump sum in exchange for a percentage of future sales.

How it’s structured:

- Funding amount: Based on monthly revenue

- Repayment: Daily or weekly automated deductions

- Term: Flexible (depends on sales volume)

- Credit: Soft pull or no hard inquiry

Why it’s popular in 2026:

- Fast approvals (same day possible)

- Minimal paperwork

- Works for bad credit

- Adjusts naturally with revenue fluctuations

Best for:

Retail, restaurants, trucking, e-commerce, home services

2. Revenue-Based Financing (RBF)

What it is:

Similar to an MCA, but structured more cleanly and often with fixed caps and longer terms.

How it’s structured:

- Repayment tied to monthly revenue

- Fixed total payback amount

- No equity given up

- Often no personal guarantee

Why it’s growing in 2026:

- Predictable repayment ceiling

- Flexible cash-flow alignment

- Startup-friendly for digital businesses

Best for:

SaaS, e-commerce, agencies, online brands

3. Business Lines of Credit (Non-Bank)

What it is:

A revolving credit line businesses can draw from as needed.

How it’s structured:

- Credit limit: Based on cash flow

- Interest: Charged only on used funds

- Repayment: Weekly or monthly

- Reusable after payoff

Why it’s favored in 2026:

- Flexible working capital

- Ideal for recurring expenses

- Lower total cost than MCAs

Best for:

Professional services, logistics, contractors

4. Short-Term Working Capital Loans

What it is:

A fixed loan with daily, weekly, or monthly payments.

How it’s structured:

- Set loan amount

- Fixed repayment schedule

- 3–24 month terms

- Faster than bank loans

Why businesses still use it:

- Simple structure

- Predictable payments

- Works for equipment or expansion

Best for:

Established businesses with steady cash flow

5. Equipment Financing & Asset-Based Funding

What it is:

Funding tied directly to equipment or hard assets.

How it’s structured:

- Equipment serves as collateral

- Lower rates than unsecured funding

- Longer repayment terms

- Easier approval than banks

Why it’s rising in 2026:

- Ideal for trucks, machinery, medical equipment

- Preserves cash flow

- Builds business credit

Best for:

Construction, trucking, healthcare, manufacturing

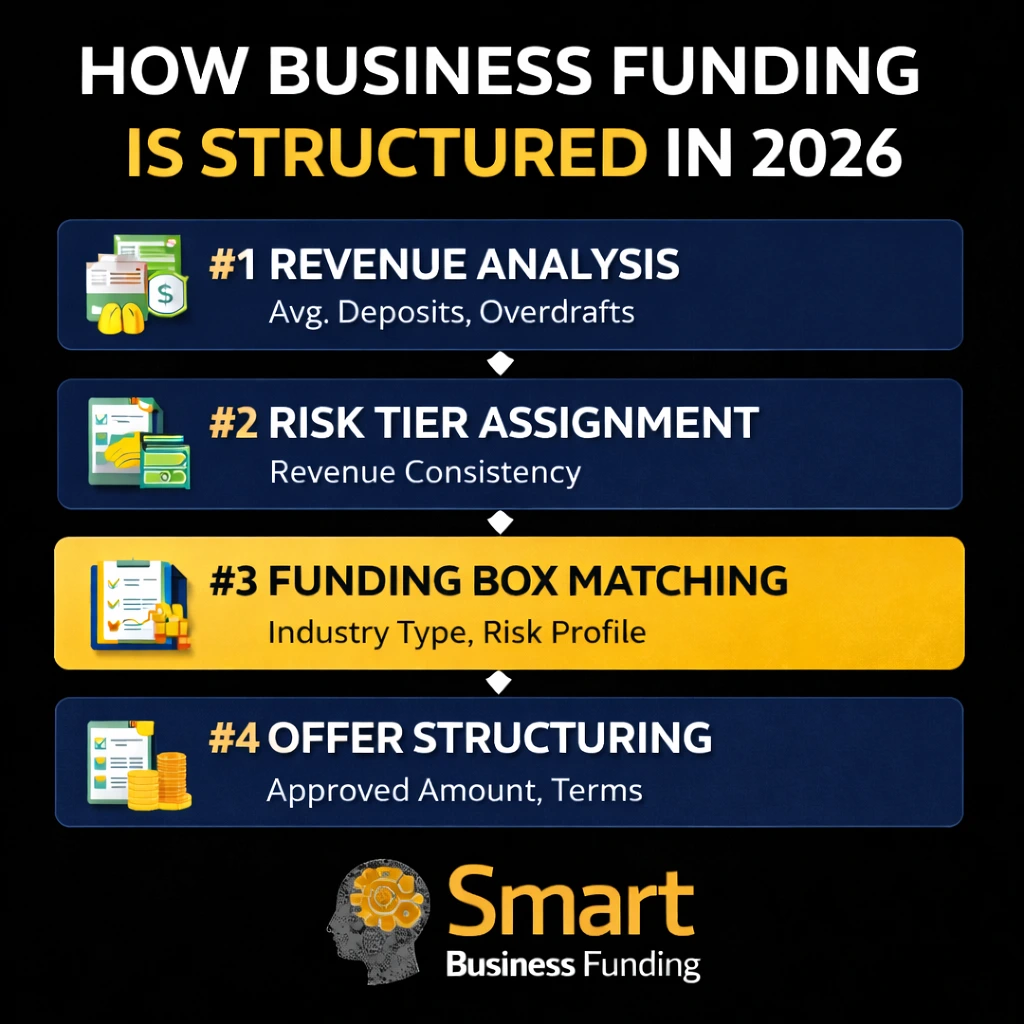

How Lenders Actually Structure Your Offer in 2026

Here’s what happens behind the scenes when you apply:

Step 1: Revenue Analysis

Lenders analyze:

- Average monthly deposits

- Revenue trends

- Deposit consistency

- Overdraft history

Step 2: Risk Tier Assignment

Your business is placed into a risk tier based on:

- Cash flow stability

- Industry type

- Time in business

- Existing funding positions

Step 3: Funding Box Matching

Each lender has a “box” — meaning:

- Minimum revenue

- Max exposure

- Industry preferences

- Term length rules

You’re matched to the best box, not the cheapest money.

Step 4: Offer Structuring

Your funding offer is built around:

- Amount approved

- Total payback

- Daily or weekly payment

- Term length

- Renewal eligibility

What Really Determines Your Approval in 2026

Forget the myths. In 2026, these five factors matter most:

- Monthly revenue (king)

- Deposit consistency

- Negative days in your bank account

- Existing advances or loans

- Industry risk profile

Credit score? It matters — but it’s no longer the deal-breaker it once was.

Daily vs Weekly Payments: How Structures Differ in 2026

Daily Payments

- Lower total cost

- Faster payoff

- Easier approval

- Better for high-volume businesses

Weekly Payments

- Higher flexibility

- Better for service businesses

- Easier cash-flow planning

- Often slightly higher cost

Why Speed Is Built Into Funding Structures Now

In 2026, funding speed is no longer a luxury — it’s a necessity.

Most modern funders now structure deals to allow:

- Same-day approvals

- 24-hour funding

- Minimal documentation

- Automated bank verification

- Digital contracts

This isn’t generosity. It’s competition. Funders that move slow lose deals.

The Biggest Mistake Business Owners Make With Funding Structures

They choose the cheapest money, not the smartest structure.

A cheaper deal that strangles cash flow can kill your business faster than a slightly higher-cost deal that gives you breathing room.

The smartest business owners in 2026 choose funding based on:

- Cash flow impact

- Growth potential

- Renewal opportunities

- Flexibility

Not just rate.

Final Thoughts: Business Funding Is a Strategy Now, Not a Last Resort

In 2026, business funding is no longer about survival — it’s about positioning.

The companies that win are the ones that:

- Secure capital before they need it

- Use funding for growth, not emergencies

- Build relationships with direct funders

- Refinance strategically at 40–60% paydown

Understanding how business funding is structured in 2026 gives you a massive edge.

Ready to Explore Your Funding Options?

Smart Business Funding works directly with businesses across every major industry, offering:

- Fast approvals

- Flexible funding structures

- Multiple position options

- Soft credit pulls

- Refinancing at 50% paid down

👉 Get pre-qualified today and see how much your business qualifies for in 2026.