Where It All Began: The Untold Story of Merchant Cash Advances

Before they became a lifeline for small business owners, Merchant Cash Advances (MCAs) were a bold, new experiment in business funding. Today, they’re a $20+ billion industry—but how did they get here? Let’s dive into the surprising, quirky, and fascinating history behind MCAs—and how they quietly revolutionized business financing.

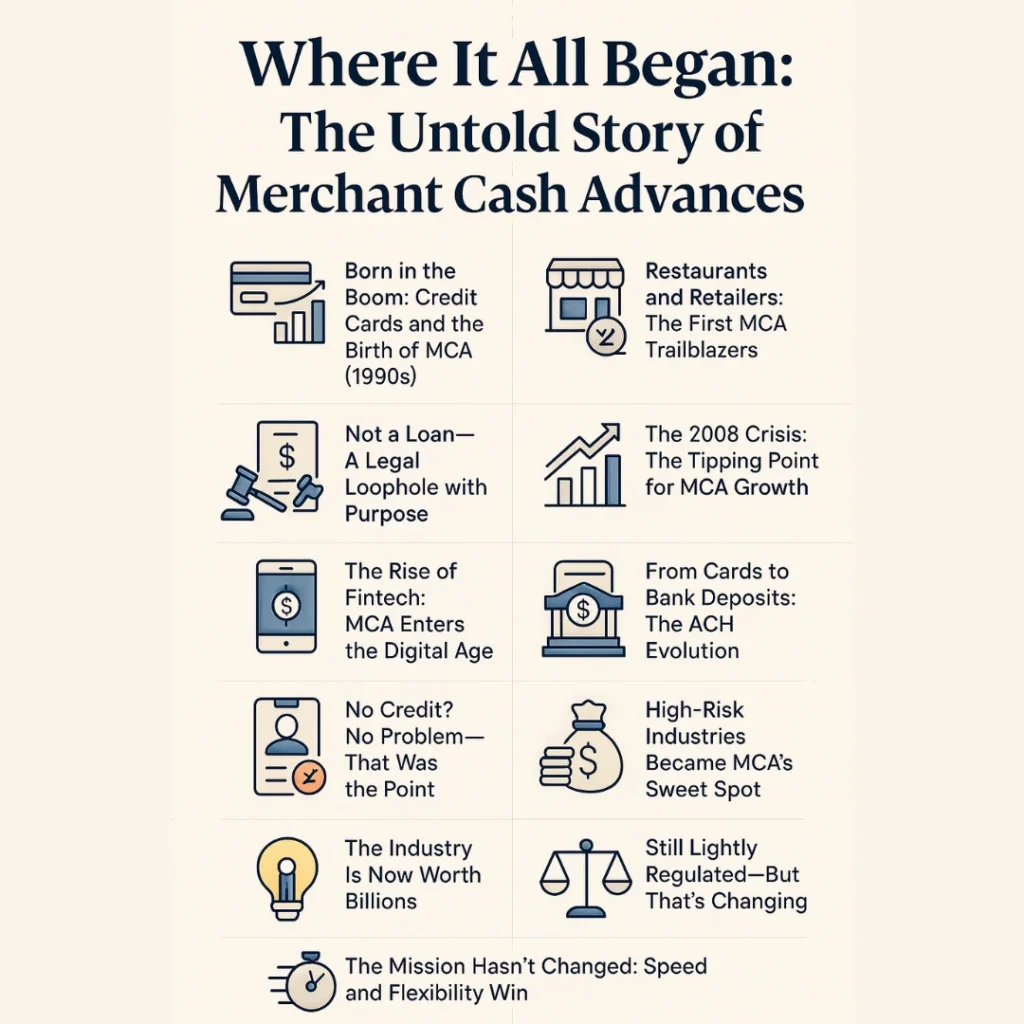

💳 1. Born in the Boom: Credit Cards and the Birth of MCA (1990s)

It all started in the late 1990s, when credit card usage exploded across the U.S. As consumers shifted from cash to plastic, small businesses—especially in retail and hospitality—suddenly had daily streams of card-based revenue.

That’s when a few visionary funders saw an opportunity. What if you could offer upfront capital to a business and get paid back through a slice of their future credit card sales?

Thus, the first MCAs were born—not as loans, but as purchases of future receivables.

📌 Example: A small café in Manhattan might receive $25,000 upfront and agree to give 15% of its daily card sales until it repays $30,000. No fixed term. No traditional interest. Just a bet on future revenue.

🛍️ 2. Restaurants and Retailers: The First MCA Trailblazers

Long before tech platforms or fintech apps, MCAs were a Main Street phenomenon. The early adopters were restaurants, bars, salons, and convenience stores—small businesses that processed credit cards but struggled to qualify for bank loans.

Traditional banks required tax returns, credit scores, and collateral. But these businesses often lacked the paperwork, and needed fast capital—for inventory, renovations, or just payroll.

📌 Real Story: In 2003, a NYC pizzeria owner reportedly turned to an MCA after being rejected by multiple banks. The MCA helped him renovate, add outdoor seating, and boost sales during the summer rush. That word-of-mouth story spread like wildfire among local entrepreneurs.

🏛️ 3. Not a Loan—A Legal Loophole with Purpose

Unlike loans, MCAs are structured as purchases of future receivables, not debt. That’s not just semantics—it was a strategic move.

Because they weren’t classified as loans, MCA providers avoided state lending laws and usury caps. This flexibility allowed them to serve “unbankable” businesses faster and with fewer restrictions.

📖 Legal Reference: In K9 Bytes, Inc. v. Arch Capital Funding, a New York court upheld that a true MCA is not a loan if there’s no absolute obligation to repay, reinforcing the product’s legal foundation as a sale, not a debt.

💥 4. The 2008 Crisis: The Tipping Point for MCA Growth

When the 2008 financial crisis hit, banks froze lending—especially to small businesses. Approval rates dropped to record lows, and Main Street felt abandoned.

Enter MCAs.

With fast approvals, minimal paperwork, and no collateral needed, MCAs filled the gap—and grew exponentially.

🔍 Stat: A 2009 Wall Street Journal report noted that while small business bank lending dropped 18% that year, MCA funding increased by over 40%.

📲 5. The Rise of Fintech: MCA Enters the Digital Age

By the mid-2010s, the fintech wave had arrived. Startups began leveraging data, automation, and APIs to underwrite risk in new ways. MCA platforms emerged with online applications, instant approvals, and real-time revenue tracking.

📌 Example: Companies like Square Capital and Shopify Capital launched their own MCA-style funding products—offering working capital based on sales data from their own platforms.

This meant any business with digital revenue could qualify for capital in hours, not weeks.

🏦 6. From Cards to Bank Deposits: The ACH Evolution

Originally, MCA providers collected repayments via card processors, pulling a percentage of credit card sales. But this limited their reach to retail-heavy industries.

With the rise of ACH (Automated Clearing House) payments, MCAs could now withdraw fixed amounts daily or weekly directly from a business bank account—opening the door to service industries, B2Bs, and beyond.

📌 Example: A home cleaning business with mostly cash or check transactions could now qualify—because their bank deposits showed revenue, even without credit card processing.

💸 7. No Credit? No Problem—That Was the Point

Early MCA providers didn’t care much about credit scores. They looked at sales volume, revenue consistency, and business activity.

This was huge for business owners with bad credit, past bankruptcies, or limited history—groups typically shut out by banks.

📌 Real Story: A mechanic in Atlanta with a 580 credit score was denied three times by banks. An MCA provider reviewed his daily deposits and approved him for $40,000—funded in 48 hours.

🏗️ 8. High-Risk Industries Became MCA’s Sweet Spot

MCA providers soon found a niche in high-risk, high-cash-flow sectors: construction, auto repair, trucking, salons, and health clinics. These businesses were growing—but banks wouldn’t touch them.

📌 Stat: According to a 2021 deBanked report, over 60% of MCA volume goes to “non-bankable” industries, proving its critical role in underserved markets.

📈 9. The Industry Is Now Worth Billions

Fast forward to today, and MCAs are no longer niche. Analysts estimate the MCA industry processes over $20 billion annually in the U.S. alone.

Big names like PayPal, Amazon, Square, and Kabbage now offer MCA-like products, and thousands of independent providers operate nationwide.

📖 Source: PYMNTS.com projects revenue-based financing (including MCAs) to grow 22% annually over the next five years.

📚 10. A New Name Game: Cash Flow Advances, Revenue Financing, and More

To avoid confusion with payday loans or predatory products, many MCA providers now rebrand as:

- “Revenue-Based Financing”

- “Cash Flow Advance”

- “Working Capital Advance”

Though the core product is similar, these names often signal transparent terms and tech-enabled platforms.

⚖️ 11. Still Lightly Regulated—But That’s Changing

Since MCAs aren’t loans, they’ve historically escaped strict federal regulation. But state laws are catching up. New laws in New York, California, and Utah now require MCA providers to disclose APR equivalents, repayment terms, and fees.

📖 Source: New York’s Commercial Finance Disclosure Law (CFDL) went into effect in 2023, signaling a new era of transparency in alternative funding.

🧠 12. The Mission Hasn’t Changed: Speed and Flexibility Win

Despite all the evolution—from analog card splits to digital fintech—MCAs have stayed true to one goal: get small business owners fast capital without the red tape.

That’s why they’re still winning in 2025.

📌 Real Story: A florist in Houston needed $15,000 to stock up for Valentine’s Day after her supplier doubled prices. Her MCA application was approved the same day—and she made 3x ROI on the investment.

✅ From a Niche Tool to a Business Lifeline

Merchant Cash Advances were born out of necessity, shaped by crisis, and fueled by innovation. What started as a workaround for card-based businesses is now a go-to funding solution for millions of entrepreneurs.

Whether you’re opening your second location, replacing a busted HVAC system, or just getting through a slow month—MCA might just be the funding solution your business story needs next.