How to Choose Between a Merchant Cash Advance, Line of Credit, or Equipment Financing

I. Introduction

For small business owners, the question isn’t “Do I need funding?”—it’s “Which funding option should I choose?”

From hiring staff to upgrading equipment to covering seasonal slowdowns, having access to capital is essential for growth. But with so many small business funding options—including merchant cash advances (MCAs), lines of credit (LOCs), and equipment financing—it’s easy to feel overwhelmed.

The truth? Each option has its strengths, weaknesses, and ideal scenarios. The right choice depends on your cash flow, urgency, credit profile, and business goals. In this guide, we’ll break down each funding type, compare them side-by-side, and give you a decision framework so you can confidently choose the best business financing option for your needs.

By the end, you’ll know not only how they work, but also why many small businesses end up choosing an alternative business financing solution—like an MCA—over traditional bank products.

II. What Is a Merchant Cash Advance (MCA)?

A merchant cash advance isn’t technically a loan—it’s an advance on your future sales. The MCA provider gives you a lump sum of working capital for small business needs, and you repay it as a percentage of your daily or weekly sales.

How It Works:

- You apply with basic financial documents (bank statements, sales history).

- Approval is often based more on sales volume than credit score—making it accessible even for those with bad credit.

- Once approved, you get fast business funding—often in 24–48 hours.

- Repayment is automatic and tied to your revenue flow.

Ideal Use Cases:

- Covering emergency expenses

- Funding marketing campaigns that can drive immediate sales

- Taking advantage of a sudden growth opportunity

- Managing cash flow during seasonal slowdowns

Pros:

- Fast business funding—much quicker than a bank loan or line of credit.

- Unsecured business funding—no collateral required.

- Flexible usage: spend on payroll, inventory, repairs, marketing, or anything else your business needs.

- Approval even with less-than-perfect credit.

Cons:

- Higher cost compared to traditional loans.

- Repayment is tied to sales, so during slow months your payments decrease, but the term can extend.

If speed, flexibility, and accessibility matter most, an MCA often wins in the merchant cash advance vs line of credit debate—especially for businesses that can’t wait weeks for approval.

III. What Is a Business Line of Credit (LOC)?

A business line of credit is like a credit card for your business—without the physical card. You’re approved for a set credit limit, and you draw funds when needed. You only pay interest on the amount you use.

How It Works:

- Apply with detailed financial statements, credit reports, and often collateral.

- Approval time can range from a few days to several weeks.

- Once set up, you can draw funds as needed for short-term business funding solutions.

Ideal Use Cases:

- Covering seasonal business funding options like stocking up for the holidays.

- Managing payroll during slower months.

- Bridging short-term gaps in accounts receivable.

Pros:

- Flexible withdrawals up to your limit.

- Only pay interest on the funds you use.

- Can be reused without reapplying (revolving credit).

Cons:

- Slower approval than an MCA.

- Requires stronger credit and financials.

- Lenders may reduce or freeze your limit if your revenue drops.

In a business line of credit vs MCA comparison, LOCs work well for businesses with predictable cash flow and solid credit—but they’re not ideal for urgent funding needs.

IV. What Is Equipment Financing?

Equipment financing is specifically designed for purchasing or leasing business equipment—like machinery, vehicles, or computers.

How It Works:

- The lender covers the cost of the equipment.

- You repay over time, and the equipment itself acts as collateral.

- Once paid off, you own the equipment outright.

Ideal Use Cases:

- Buying a delivery truck for a logistics company.

- Upgrading manufacturing machinery.

- Purchasing commercial ovens for a restaurant.

Pros:

- Competitive interest rates (lower than MCAs in most cases).

- Easier approval because the asset serves as collateral.

- Helps preserve working capital for other expenses.

Cons:

- Funds can only be used for equipment—not other business needs.

- Approval may take longer than an MCA.

When it’s equipment financing vs merchant cash advance, equipment financing wins for single-purpose purchases where cost is the main concern. But if you need cash for multiple expenses (e.g., installation, training, marketing), an MCA gives more flexibility.

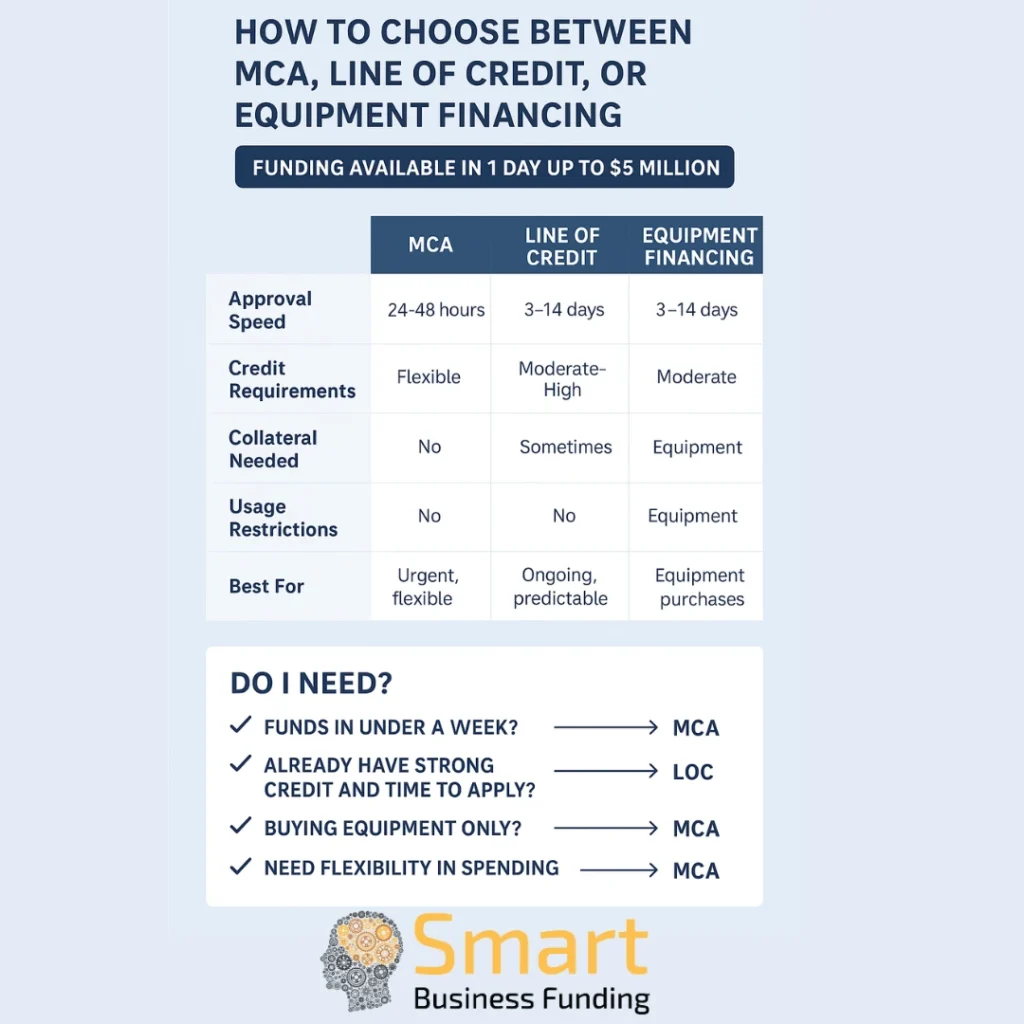

V. MCA vs LOC vs Equipment Financing: Side-by-Side Comparison Table

| Feature | MCA | Line of Credit | Equipment Financing |

|---|---|---|---|

| Approval Speed | 24–48 hours | 3–14 days | 3–14 days |

| Credit Requirements | Flexible | Moderate–High | Moderate |

| Collateral Needed | No | Sometimes | Yes (equipment) |

| Usage Restrictions | None | None | Equipment only |

| Repayment | % of daily/weekly sales | Monthly | Monthly |

| Best For | Urgent, flexible needs | Ongoing, predictable needs | Equipment purchases |

This MCA vs LOC vs equipment financing comparison makes one thing clear: If speed and flexibility are top priorities, MCA comes out ahead.

VI. Which Option Fits Your Business Scenario?

Scenario 1: Seasonal Cash Flow Shortage

- LOC: Works if you have a strong credit history and can plan ahead.

- MCA: Works if you need funds immediately to stock inventory or cover payroll.

Scenario 2: Emergency Repairs/Upgrades

- MCA: Best for urgency—you can get funded in 1–2 days.

- LOC: Viable if already set up in advance.

Scenario 3: Buying New Equipment

- Equipment Financing: Ideal if the purchase is the only need.

- MCA: Useful if you also need cash for installation, training, or marketing.

When deciding which is better: MCA or line of credit, ask yourself: Do I need the money now, and do I want freedom to use it however I choose? If the answer is yes, MCA is often the smarter choice.

VII. Calculating the ROI for Each Option

The cost of capital matters—but so does the return it enables.

Simple ROI Formula:

ROI (%) = (Net Profit from Investment – Cost of Financing) ÷ Cost of Financing × 100

Example:

You spend $20,000 on a marketing campaign funded by an MCA.

- Campaign generates $50,000 in sales.

- Net profit after expenses = $25,000.

- MCA cost (factor rate) = $4,000.

ROI = (25,000 – 4,000) ÷ 4,000 × 100 = 525%

When viewed this way, MCA’s higher cost can still make sense if it enables fastest funding for equipment upgrades or immediate business expansion financing that delivers big returns.

VIII. Common Misconceptions About MCAs

Myth 1: “MCAs Are Just Expensive Loans”

- Truth: MCAs are alternative business financing—structured differently from loans, with repayment tied to revenue.

Myth 2: “Only Struggling Businesses Use MCAs”

- Truth: Many profitable businesses use MCAs for growth because they provide unsecured business funding without collateral.

Myth 3: “Factor Rates Are Just High Interest Rates”

- Truth: Interest rates vs factor rates are calculated differently; MCAs charge a fixed fee instead of compounding interest.

By reframing these misconceptions, business owners can see MCAs as strategic tools rather than last-resort funding.

IX. Final Decision Framework

Checklist:

- Need funds in under a week? → MCA.

- Already have strong credit and time to apply? → LOC.

- Buying equipment only? → Equipment financing.

- Need flexibility in spending? → MCA.

- Have seasonal cycles but can plan ahead? → LOC.

This framework ensures you choose the best business financing option for your situation without second-guessing yourself.

X. Conclusion + CTA

Choosing between a merchant cash advance, line of credit, or equipment financing isn’t about which one is “best” in general—it’s about which one is best for your current goals, timeline, and cash flow.

If your priority is fast business funding, flexibility in how you use the money, and a streamlined approval process—even with less-than-perfect credit—an MCA can be the ideal fit.

Ready to see how much you qualify for?

Get your same-day MCA quote now and secure the working capital your business needs—without the wait, without the red tape.